COVID 19 EMPLOYMENT LAW SUPPORT

INSTANT ACCESS TO OUR EXPERTS.

NO LONG TERM FIXED CONTRACT

Furlough under the Coronavirus Job Retention Scheme (Original form)

FAQs last updated: 16/06/2020

NOTE – these FAQs concern the Coronavirus Job Retention Scheme in its original form and will not be updated further. We provide a high level summary of the forthcoming changes to the Scheme at question 2(a) of these FAQs. However, for details of these changes (that will take effect from 1 July), please refer to our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, which we will continue to update as any further guidance becomes available.

1. What is Furlough Leave? (Last updated 16/06/2020)

Furlough leave is a form of leave which the Government has made available to UK businesses via its Coronavirus Job Retention Scheme (the ‘Scheme’).

The Scheme was announced by the Chancellor on Friday 20 March as part of a package of “temporary, timely and targeted measures to support public services, people and businesses through this period of disruption caused by Covid-19”. The Scheme was originally intended to run for at least 3 months from 1 March, but the Government said it would be extended if necessary. On 17 April, the Chancellor announced an extension of the Scheme to the end of June. On 12 May, the Government announced that the Scheme will continue until the end of October (the ‘Further Extension’), with some adjustments which will take effect from August to allow new flexibility (the ‘Revised Scheme’). The Government hopes that these adjustments will help to get employees back to work and boost the economy. See question 2(a), below, for a high level summary of the Revised Scheme, and our ‘Furlough under the Revised Coronavirus Job Retention Scheme’ FAQs for further detail.

1(a). What official guidance is there on the Scheme? (Last updated 16/06/2020)

Government guidance on the Scheme was first published on 26 March and has been through numerous iterations since then. The latest Government guidance on the Scheme for employers is set out across a number of webpages, all of which can be accessed from this central guidance hub page.

Specific guidance on holiday entitlement and pay during coronavirus, which deals with holidays for all employees, both those who are working and those who are on furlough, was published on 13 May.

A Treasury Direction setting out certain technical details of the Scheme was published on 15 April. There were some significant inconsistencies between the initial version of the Treasury Direction and the Government guidance. An amended Treasury Direction was published on 22 May, which resolves some of these issues, but we think that there are various points of difficulty remaining. (Note that claims made on or after 23 May must be in accordance with the amended Treasury Direction.)

Where there are inconsistencies between the Government guidance and the Treasury Direction, from a legal perspective, we would expect that the Treasury Direction would be accorded more weight. This is because, while it is not a piece of legislation, it is an exercise of ministerial authority conferred by an Act of Parliament and is legislative in nature. Some of the amendments that were made to the Government guidance after the initial version of the Treasury Direction was published appeared to reinforce the differences between these two sources of information on the Scheme, which we thought suggested that, where they were inconsistent, HMRC may not have been intending strictly to enforce the requirements of the Treasury Direction. However, now that a new version of the Treasury Direction has been published, we think it likely that HMRC would resolve any remaining inconsistencies in favour of the Treasury Direction, rather than the Government guidance, at least as far as the operation of the Scheme in its initial form is concerned.

We also expect the Treasury Direction to be updated again to reflect the Further Extension in due course.

2. In summary, how does the Scheme work? (Last updated 01/06/2020)

The Government guidance for employers states that the Scheme is designed to help all UK businesses who cannot maintain their current workforce because their operations have been severely affected by coronavirus (COVID-19). There is no guidance around how this will be assessed, so employers will need to apply their own judgement/discretion about whether the scheme is intended for them. However, the Government guidance does expressly state that different businesses will face different impacts from coronavirus.

We appreciate that, in the absence of any detailed explanation as to the meaning of ‘severely affected’, it will not be straightforward for companies to determine whether they are eligible to access the Scheme. We note that the Treasury Direction (both the original and the amended version) does not reflect the language used in the Government guidance. It refers to the purpose of the Scheme being to provide for payments to employers in respect of costs of employment incurred in respect of furloughed employees “arising from the health, social and economic emergency in the United Kingdom resulting from coronavirus and coronavirus disease”. Although it appears quite broad, this statement does not shed any further light on the extent to which an employer’s business must have been affected in order to legitimately access the Scheme and we do not think it removes this requirement. It is also worth noting that the Treasury Direction states that claims will not be permitted where they are “abusive” or “otherwise contrary to the exceptional purpose” of the Scheme, and the Government guidance emphasises the fact that HMRC will check claims made through the Scheme. It specifies that payments may be withheld or need to be repaid in full to HMRC if the claim is based on dishonest or inaccurate information, or is found to be fraudulent. In addition, the Government guidance for employees includes a link for reporting suspected fraud by employers.

A furloughed employee remains on the employer’s payroll, so furlough leave is a form of authorised absence. The guidance provides that furlough leave must be for a minimum of three consecutive weeks.

To be eligible under the Scheme an employer must have created and started a PAYE payroll scheme on or before 19 March 2020, enrolled for PAYE online (which can take up to 10 days), and have a UK bank account. Any entity with a UK payroll can apply, including businesses, charities, recruitment agencies and public authorities. Note that where a group of companies has multiple PAYE schemes and there is a transfer of all employees from these schemes into a new consolidated PAYE scheme after 19 March 2020, the new scheme will be eligible to furlough those employees and claim the grants available under the Scheme.

The existing terms of the Scheme enable employers to claim for 80% of furloughed employees’ usual/regular monthly wage costs, up to £2,500 a month, plus the associated Employer National Insurance contributions and minimum automatic enrolment employer pension contributions on that subsidised furlough pay. An employer can choose to fund the difference between the 80% / £2,500 payment and an employee’s full salary, but there is no requirement to do so. Employees on reduced income in these circumstances may also be eligible for other support including Universal Credit.

Employers can reclaim the payments from HMRC by providing information on an online portal about employees who have been furloughed and their salaries. The portal opened for claims on 20 April and the step-by-step guide for employers indicates that payments via the portal should be made within six working days of an application being submitted. HMRC experienced high volumes of applications in the initial days of operation but seems to be coping relatively well with demand. Businesses that require an additional cash injection could access the Coronavirus Business Interruption Loan Scheme (CBILS), which is offering loans of up to £5 million for SMEs through the British Business Bank, or the Covid-19 Corporate Financing Facility. The CBILS is open for applications; details are available here.

The Government has stated that the Scheme will continue in its current form until the end of July. Then, from 1 August to the end of October, new flexibility will be introduced to the Scheme – see question 2(a), immediately below, for details of this Further Extension and Revised Scheme.

2(a). How will the Further Extension and the Revised Scheme operate and when will the changes take effect? (Last updated 16/06/2020)

As noted above, on 12 May, the Government announced that the Scheme will continue until the end of October (the ‘Further Extension’), with some adjustments which will take effect from August to allow new flexibility (the ‘Revised Scheme’). The Government hopes that these adjustments will help to get employees back to work and boost the economy. Limited further information regarding implementation of the Further Extension and the Revised Scheme was provided by the Government on 29 May in an announcement and a factsheet and we consider the implications of this below and further details of how the Revised Scheme will operate were added to the Government guidance on 12 June.

Flexibility to allow part-time work during furlough

Under the Scheme in its current form, furloughed employees are currently not allowed to perform any work for their employer (see question 18, below). This lack of flexibility has made it difficult for some businesses to get back up and running. Following lobbying by Make UK and other business groups, the Government announced that greater flexibility would be introduced to the Scheme.

From 1 July 2020, under the Revised Scheme businesses will be given the flexibility to bring furloughed employees back to work part time. It is worth highlighting that this flexibility is being introduced a month earlier than anticipated, as the original announcement had suggested it would only come into effect in August.

Employers will be able to decide the hours and shift patterns their furloughed employees will work on their return (although any contractual changes will need to be agreed and confirmed in writing). The 29 May announcement indicated that this flexibility is intended to enable employers to bring the workforce back in a staggered way while continuing to receive financial support. However, employers will be responsible for paying employees’ wages while they are in work, i.e. claims under the Revised Scheme will only cover the hours for which furloughed employees are not working.

When they make their claim, employers will be required to submit data on the usual hours a furloughed employee would be expected to work in a claim period and actual hours worked. When claiming for furloughed hours, employers will need to report and claim for a minimum period of a week at a time, in order for grants to be calculated accurately across employees’ working patterns. This is a minimum period and employers will be able to make claims for longer periods, e.g. if their employees are on monthly or two weekly cycles.

Closure of the Scheme to new entrants

Claims from July onwards will be restricted to employers who are currently using the Scheme and to previously furloughed employees. The Scheme will close to new entrants on 30 June, which means that the final date by which an employer could furlough an employee for the first time was 10 June, in order for the current minimum three-week furlough period to be completed by 30 June. Announcing this change, the Government said that such a restriction was necessary to enable the introduction of part-time furloughing and support those already furloughed back to work. There is an exemption for parents on extended leave, see below.

Note that it was not absolutely clear from the information in the Government’s announcement or the accompanying factsheet whether an employee would need to be on furlough immediately before the changes take effect in order for the employer to be able to claim for them under the Revised Scheme from 1 July onwards. Our initial reading of the limited information available was that this was not the intention and that an employee could therefore be furloughed in July even if they were not on furlough in June, provided that they had at some point previously been on furlough under the Scheme in its initial form, e.g. because the employer has been operating furlough on a rotational basis. However, this scenario was not expressly covered in the announcement or factsheet so we were unable to say this with certainty. The further guidance published on 12 June confirms our understanding, i.e. provided an employee has been on furlough for a 3 week period at any time before 30 June, they will be eligible to be furloughed under the Revised Scheme.

Another aspect of the factsheet which had caused some confusion was the statement that “[T]he number of employees an employer can claim for in any claim period cannot exceed the maximum number they have claimed for under any previous claim under the current CJRS”. It was not immediately clear whether this provision would impact on a company that had, for example, previously been operating rotational furlough (e.g. keeping half the workforce on furlough for three weeks, with the other half working and then swapping them over) but in July wished to change so that all of the workforce work on a part-time basis and receive furlough pay for their remaining hours not worked. Such a change might potentially involve claiming for more employees in a single claim than the employer had done previously. On the basis of the further guidance published on 12 June, it appears that such a change will therefore not be permitted, as that guidance states: “For example, an employer had previously submitted three claims between 1 March 2020 and 30 June, in which the total number employees furloughed in each respective claim was 30, 20 and 50 employees. Then the maximum number of employees that employer could furlough in any single claim starting on or after 1 July would be 50.” Employers will need to bear this restriction in mind when determining how they make use of the Revised Scheme from July. (However, there are exceptions to the cap where an employer is furloughing for the first time employees who have previously been on family leave, or who transferred under TUPE after 10 June.)

Employers will have until 31 July to make any claims under the Scheme in respect of the period to 30 June. Once the changes take effect, employers will still be able to make claims in anticipation of an imminent payroll run, at the point payroll is run or after payroll has been run. They will be able to make their first claim under the Revised Scheme from 1 July. From 1 July, claim periods will no longer be able to overlap months. Employers who previously submitted claims with periods that overlapped calendar months will no longer be able to do this going forward. The factsheet states that this is necessary to reflect the forthcoming changes to the Scheme.

Parents on family leave who return to work in the coming months can be furloughed and are exempt from the 10 June cut-off date, provided the employer has previously furloughed other employees. This exemption applies to those on maternity, paternity, adoption leave, shared parental leave and parental bereavement leave. There is also an exception where employees transfer to a new employer under TUPE after 10 June, provided that they have previously been furloughed by their old employer. In addition, on 15 June, the Government announced an exception for reservist servicemen and servicewomen who come back to their day job after completing a period of active duty. They will be able to be furloughed by their employer for the first time under the Revised Scheme, provided their employer has previously furloughed other employees. We cover these exceptions in greater detail in our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’.

Gradual reduction in level of financial support

The amount that employers can claim under the Scheme will remain the same during June and July (although if you are bringing employees back part-time in July, only their non-working (or furloughed) hours will be covered and the monthly cap on furlough pay will be proportional to the hours not worked).

Going forwards, in addition to the tapering of support described below, if your furloughed employees are working part-time under the Revised Scheme, the amount of furlough pay you can claim will only cover non-working hours and the monthly cap on furlough pay will be proportional to the hours not worked. You will be responsible for paying the employees for their working hours.

From 1 August 2020, the level of Government grant will be slowly tapered, but employees will continue to receive 80% of their normal pay (subject to a monthly cap of £2,500) covering the time they are unable to work.

During August, employers will be able to claim 80% of furloughed employees’ wages up to a monthly cap of £2,500 under the Revised Scheme. However, employers will no longer be able to claim for employer NICs or pension contributions under the Revised Scheme and will have to fund these themselves.

During September, employers will be able to claim 70% of furloughed employees’ wages up to a monthly cap of £2,190 under the Revised Scheme. As well as employer NICs and pension contributions, employers will have to fund 10% of the normal wages received by furloughed employees, so that the employees continue to receive 80% of their pay, up to the monthly cap of £2,500.

During October, employers will be able to claim 60% of furloughed employees’ wages up to a monthly cap of £1,875 under the Revised Scheme. As well as employer NICs and pension contributions, employers will have to fund 20% of the normal wages received by furloughed employees, to make up the 80% total to which the employees are entitled subject to the monthly cap of £2,500.

3. Who can be furloughed? (Last updated 16/06/2020)

Note, in view of the changes to the Scheme summarised at question 2(a), above, it is no longer possible to furlough any employee for the first time after 10 June (except for those who have been on maternity, paternity, adoption leave, shared parental leave and parental bereavement leave, where you have previously furloughed other employees). The content below explains the other eligibility conditions for furlough. For details of furlough from 1 July, see our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’.

Furloughed employees must have been on the employer’s PAYE payroll on or before 19 March 2020, and can be on any type of employment contract, including:

- full-time employees

- part-time employees

- employees on flexible or zero-hour contracts

- apprentices

- employees on fixed term contracts

In respect of employees on fixed-term contracts, their contracts can be renewed or extended during the furlough period without breaking the terms of the Scheme. See question 5, below, for the position where a fixed-term employee’s contract has ended.

In addition, the following categories of individuals are also eligible if they are paid by PAYE and were on payroll on or before 19 March:

- Office holders (including company directors).

- Agency workers whether or not they are employees of the agency, including those employed by umbrella companies. For all agency workers, furlough should be agreed between the agency and the worker, or where there is an umbrella company, the umbrella company and the worker.

- Limb (b) workers (sometimes known as dependant contractors, where the individual carries out work or services for another party who is not their client or customer), unless they pay tax on their trading profits through Income Tax Self-Assessment, in which case they may be eligible for the Self-Employed Income Support Scheme.

- Salaried members of Limited Liability Partnerships who are designated as employees for tax purposes (‘salaried members’) under the Income Tax (Trading and Other Income) Act (ITTOIA) 2005.

Note too that foreign nationals are eligible to be furloughed. Grants under the scheme are not counted as ‘access to public funds’, and you can furlough employees on all categories of visa. This includes employees who are on Tier 2 visas and those who are in the process of applying for indefinite leave to remain (ILR). However, for such employees, their furlough pay may be lower than their minimum visa salary threshold, or minimum ILR salary bands. Accordingly, it is important that their pay returns to previous levels once the impact of Covid-19 has passed. For employees whose visas are due to expire between March and July, the Home Office have extended the visa application deadline.

It is important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. See question 2(a), above, for further details.

4. Can an employer furlough recent starters? (Last updated 16/06/2020)

Note, in view of the changes to the Scheme summarised at question 2(a), above, it is no longer possible to furlough any employee for the first time after 10 June (except for those who have been on maternity, paternity, adoption leave, shared parental leave and parental bereavement leave, where you have previously furloughed other employees). The content below explains the other eligibility conditions for furlough. For details of furlough from 1 July, see our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’.

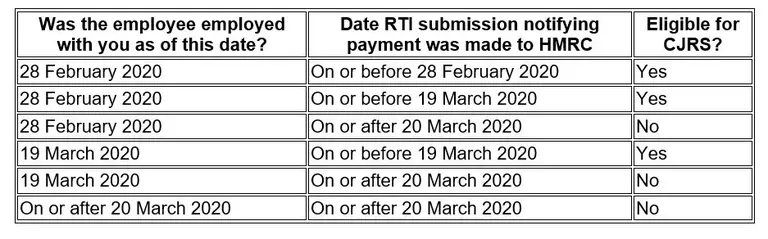

You can only furlough employees who have been on your payroll since 19 March 2020 and which were notified to HMRC on an RTI submission on or before 19 March 2020. This means an RTI submission notifying payment in respect of that employee to HMRC must have been made on or before 19 March 2020. Employees who were placed on your payroll/in respect of whom an RTI submission was made to HMRC only after 19 March 2020 cannot be furloughed or claimed for under the Scheme.

Note that earlier Government guidance on the Scheme had set the date at which employees had to have been on payroll in order to be claimed for at 28 February 2020. This was considered necessary in order to protect against fraudulent claims (e.g. an employer taking on friends/family simply in order to furlough them and claim furlough pay from HMRC). However, following significant public pressure identifying the unfairness this created for employees who had started genuine new jobs in March, the Government guidance was amended on 15 April. The eligibility date of 19 March is the day before the Scheme was first announced – thus still preventing the sort of fraudulent claim described above.

While the extension of the Scheme to employees who were on payroll on 19 March will cover a significant number of new starters, it will not necessarily cover everyone. This is because eligibility is contingent on the employer having made an RTI submission for the employee on or before 19 March, and monthly paid employees who started work in advance of 19 March will not have been paid until the March payroll. Most employers who run a monthly payroll process payments at or around the end of the month, so the RTI submission for these employees is likely to fall after the cut-off date of 19 March. We do not think that there will be any further movement on this from HMRC, since the requirement to have made an RTI submission in respect of the employee is expressly set out in the Treasury Direction, although we are raising the point with Government.

While there is no obligation on them to do so, it is open to employers who wish to protect their new starters who are still not covered by the Scheme to fund a period of authorised leave equivalent to furlough themselves, if they can afford this.

Many employers will have placed employees whom they took on after 28 February, who were not previously covered by the Scheme, on unpaid lay-off. If those employees would now be covered following the extension of the cut-off date to 19 March, the employer could consider moving them to furlough leave going forwards (although note that if an employer has not done so already, it would need to do this by 10 June due to the forthcoming closure of the Scheme to new entrants – see further below, and at question 2(a), above).

The 23 April update to the Government guidance includes a helpful table identifying the dates that employees must have been on your PAYE payroll and an RTI submission made in order to be eligible under the Scheme:

5. What about employees who have already left the business? (Last updated 16/06/2020)

Note, in view of the changes to the Scheme summarised at question 2(a), above, it is no longer possible to furlough any employee for the first time after 10 June (except for those who have been on maternity, paternity, adoption leave, shared parental leave and parental bereavement leave, where you have previously furloughed other employees). The content below explains the other eligibility conditions for furlough. For details of furlough from 1 July, see our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’.

You can use the Scheme to furlough employees who have left the business since 28 February 2020, if you re-hire them. The Government guidance that appears under the heading “If you made employees redundant or they stopped working for you on or after 28 February” states that this applies to employees that were made redundant or stopped working for you after 28 February, even if you do not re-employ them until after 19 March, as long as the employee was on your payroll as at 28 February and had been notified to HMRC on an RTI submission on or before 28 February 2020.

A further update to the Government guidance made on 23 April deals expressly with the position of employees who were made redundant or stopped working for you after 19 March 2020. It specifies that these employees can be rehired and furloughed provided that they were employed on or before 19 March 2020, were on your PAYE payroll on or before 19 March 2020 and an RTI submission was made in respect of them on or before 19 March 2020. This addition removes the uncertainty that previously existed around whether you could rehire and furlough employees who had left the business after 19 March (i.e. after the Scheme was announced).

(Note, that while the Treasury Direction does not deal directly with rehiring employees who have left the business in order to furlough them, it does provide that an employee will only count as a furloughed employee if (among other things), the instruction not to work is given “by reason of circumstances arising as a result of coronavirus or coronavirus disease”. This calls into question whether an employer can rehire and furlough an employee in all circumstances. For example, it is doubtful an employer could rehire and furlough someone it had made redundant for a reason unrelated to Covid-19, since the reason the employer would have no work for them to do is that their position was already redundant notwithstanding the coronavirus crisis. This apparent restriction does seem at odds with other announcements on the Scheme and we hope that the position will be clarified by the Government).

If you decide to re-hire any former employees, you would need to contact them, seek their agreement to be re-employed and then their consent to being furloughed. We had previously understood that furlough leave for employees you rehired and furloughed in this way could be backdated to the later of the date their employment terminated, or 1 March 2020. However, the update to the Government guidance on 17 April indicates that you can only claim for these employees’ wages under the Scheme from the date on which you furlough them through the Scheme. (See further question 13(f) below, for more details on the uncertainty surrounding the issue of backdating.)

If you rehire an employee whose employment terminated more than a week before, the ordinary position would be that their continuity of employment has been broken, and it is not possible for an employer and employee to preserve continuity by agreement. Accordingly, to ensure fairness to the employee, you may wish to allow them to retain any termination payment they received, e.g. redundancy pay, as they will not qualify for this again if they are subsequently dismissed as redundant when the Scheme comes to an end. (Note that there may potentially be scope for an employee to argue that continuity was not actually broken, on the basis that the gap between contracts constituted a “temporary cessation of work”. The case law in this area indicates that whether a cessation was temporary will be considered retrospectively, with the benefit of hindsight, but the expectations of the parties at the time the first contract ended will be relevant. Each case will depend on the individual circumstances. We therefore suggest that you seek advice if you are considering rehiring an employee who had left in order to access the Scheme and you are concerned about continuity).

You are not obliged to rehire any employees who have left the business since 28 February 2020. If you do rehire, remember that at the end of the furlough period, these individuals would remain employed by you. If redundancies are necessary at that point, you would need to start a new redundancy process. To avoid these potential complications, you could agree with the employee when you rehire them that their re-engagement will be for a fixed term and will terminate when the Scheme ends. The changes to the Scheme that will require employers to make some contribution towards the cost of employees’ furlough pay from August 2020 mean that you may wish to consider how long you are willing to keep employees whom rehire on furlough. If you have already rehired employees you may wish to review the terms of any fixed term contract.

Note also that the Government guidance specifies that if an employee has had multiple employers over the past year, has only worked for one of them at any one time, and is being furloughed by their current employer, their former employer(s) should not re-employ them, put them on furlough and claim for their wages through the scheme.

With regard to a fixed-term employee whose contract ended because it was not extended or renewed before its natural conclusion, you can rehire and furlough the employee provided that either:

- their contract expired on or after 28 February 2020 and an RTI submission was notified to HMRC on or before 28 February 2020; or

- their contract expired on or after 19 March 2020 and an RTI submission was notified to HMRC on or before 19 March 2020.

However, an employee whose contract both started and ended between 28 February 2020 and 19 March 2020 cannot be furloughed under the Scheme. This applies to both fixed-term employees and employees on other contracts.

5(a). What about employees who are currently in their notice period? (Last updated 16/06/2020)

Note, in view of the changes to the Scheme summarised at question 2(a), above, it is no longer possible to furlough any employee for the first time after 10 June (except for those who have been on maternity, paternity, adoption leave, shared parental leave and parental bereavement leave, where you have previously furloughed other employees). The content below explains the other eligibility conditions for furlough. For details of furlough from 1 July, see our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’.

Employees who are currently in their notice period are not specifically dealt with in the Government guidance. However, our view is that if an employee has resigned or been given notice of dismissal and is working out their notice period, but you now no longer have work for them to do due to Covid-19, you should be able to agree with them that they will be furloughed for the remainder of their notice period.

5(b). What about employees who transfer under TUPE? (Last updated 16/06/2020)

Note, in view of the changes to the Scheme summarised at question 2(a), above, it is no longer possible to furlough any employee for the first time after 10 June (except for those who have been on maternity, paternity, adoption leave, shared parental leave and parental bereavement leave, where you have previously furloughed other employees). The content below explains the other eligibility conditions for furlough. For details of furlough from 1 July, see our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’.

In employment law, the effect of TUPE is that post-transfer it is as if the transferred employee had always been employed by the new employer. The revised Government guidance specifies that the new employer will be allowed to claim under the Scheme in respect of the employees of a previous business who transferred to it after 28 February 2020 if either the TUPE or PAYE business succession rules apply to the change in ownership.

The amended Treasury Direction provides that where transferring employees were furloughed by the old employer pre-transfer, but have been on furlough for less than the three week minimum furlough period at the time the transfer takes place, the old employer will not be prevented from making a claim under the Scheme for the period immediately before the transfer, provided that the new employer makes a claim under the Scheme in respect of the transferring employees for the period immediately after the transfer. We assume that the new employer would have to furlough the transferring employees for at least three weeks immediately following the transfer in order for this provision to apply, since the amended Treasury Direction does not suggest that the old and new employers can aggregate the time the transferring employees spend on furlough with each of them in order to make up the minimum furlough period. It also appears from this provision that the old employer’s ability to claim under the Scheme where transferring employees were on furlough with them for less than three weeks pre-transfer will be dependent on the new employer’s actions. If the new employer has work for the transferring employees to do following the transfer and therefore does not furlough them, the old employer will be unable to claim for the period they spent on furlough before the transfer.

If a TUPE transfer is into a brand new company that did not have a PAYE payroll established as at 19 March 2020, there is guidance in the amended Treasury Direction about how the new employer can access the Scheme.

5(c). What about employees with an annual pay period? (Last updated 16/06/2020)

Note, in view of the changes to the Scheme summarised at question 2(a), above, it is no longer possible to furlough any employee for the first time after 10 June (except for those who have been on maternity, paternity, adoption leave, shared parental leave and parental bereavement leave, where you have previously furloughed other employees). The content below explains the other eligibility conditions for furlough. For details of furlough from 1 July, see our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’.

You can furlough employees – such as some company directors – who have an annual pay period, as long as they meet the relevant conditions. This includes being notified to HMRC on an RTI submission on or before 19 March 2020, which relates to a payment of earnings in the 2019 - 20 tax year. (The requirement for there to be payment of earnings in the 2019 - 20 tax year applies for any employee you claim for under the Scheme, irrespective of how frequently they are paid, e.g. weekly, fortnightly or monthly). This means that you will be unable to claim for those on an annual pay period if the last payment notified to RTI was before 5 April 2019 and no further payments were notified until after 19 March 2020.

6. Can an employer furlough those who are currently on sick leave or self-isolating? (Last updated 16/06/2020)

The Government guidance points out that the Scheme is not intended to be used by employers for short-term absences from work due to sickness. This makes sense given the three week minimum furlough period.

However, the Government guidance seems to permit an employee who is currently on short or long term sick leave to be moved onto furlough if you have a business reason for doing so. It states that in these cases, the employee should no longer receive sick pay and would be classified as a furloughed employee.

The original version of the Treasury Direction seemed to be inconsistent with the Government guidance, providing that an employee’s entitlement to SSP would need to come to an end before the employee could be furloughed. While its drafting is somewhat opaque, the amended Treasury Direction appears to be intended to iron out this inconsistency. It provides that where an employee is in receipt of (or entitled to) SSP, their furlough period cannot begin until the period of incapacity for work for which they are receiving or entitled to SSP has ended – but that the period of incapacity for work can be ended by agreement between the employer and the employee. This seems to permit an agreement whereby an employee foregoes their entitlement to SSP in order to be furloughed, even if they are not actually fit to return to work. While the flexibility this offers is helpful to employers insofar as it broadens the circumstances in which they can access the Scheme, it raises potential questions around the management of employees’ sickness absence more broadly, e.g. how does an agreement to end a period of incapacity for work in this way affect the employee’s entitlement to company sick pay? Can the employer no longer count days after such an agreement takes effect as days of sickness absence under its absence management policy, even if the employee would not in fact be fit to return to work? (See further questions 6(d), below.)

Another support measure that the Government has put in place for employers, separate from the Scheme, is a rebate system under which employers with fewer than 250 employees can claim back the cost of Covid-19-related SSP (the SSP Rebate Scheme – see the FAQs on Financial support for your business for more information). The Government guidance on the interaction between furlough and sick leave makes clear that you can claim back from both the Scheme and the SSP Rebate Scheme for the same employee but not for the same period of time. When an employee is on furlough, you can only reclaim expenditure through the Scheme, and not the SSP Rebate Scheme. The Treasury Direction does not mention the SSP Rebate Scheme, so we assume the position on this remains unchanged.

It is important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. This means that if an employee has not previously been furloughed, from July you will not be able to use furlough to cover their absence from work due to sickness. See question 2(a), above and our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, for further details.

6(a). Can an employer furlough an employee who is unable to work due to childcare needs? (Last updated 16/06/2020)

Yes. The Scheme is expressly stated to be available for those who are unable to work because they have caring responsibilities resulting from coronavirus, such as the need to look after children. This appears to be regardless of whether you would otherwise have furloughed them or had work for them to do – although, as is the case for all categories of employee, the general point that the Scheme is intended to be available to companies whose operations have been severely affected by Covid-19 would still apply (see question 2, above).

It is important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. See question 2(a), above and our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, for further details.

6(b). Can an employer furlough an employee who is shielding or who needs to stay at home with someone who is shielding? (Last updated 16/06/2020)

Yes. The Government guidance expressly states that the Scheme is available to employees who are shielding in line with public health guidance (i.e. extremely vulnerable individuals who are most at risk of suffering severe and life-threatening symptoms if they contract Covid-19 and whom the NHS has contacted individually to advise them to remain at home – although the guidance has recently been relaxed to allow these individuals to spend some time outside their home, e.g. for exercise, they are still advised to avoid contact with people outside their household and working outside the home – and current advice is that they continue to shield until at least 30 June) and those who need to stay at home with someone who is shielding.

There was some confusion following the amendments made to the guidance on 4 April which stated that you could only furlough these individuals if they were unable to work from home and you would otherwise have to make them redundant. As we hoped (and lobbied for), this was revisited by the Government in its 9 April guidance and the ‘otherwise redundant’ requirement was removed. In short, the Government guidance indicates that you can decide whether to furlough these employees – although, as is the case for all categories of employee, the general point that the Scheme is intended to be available to companies whose operations have been severely affected by Covid-19 would still apply (see question 2, above).

There had also been a degree of confusion because of regulations brought into force on 16 April which provide for individuals who are shielding to be entitled to SSP, whereas they were previously excluded. The explanatory notes to these regulations state that this SSP entitlement is intended as a safety net for shielding individuals, in cases where their employer chooses not to furlough them under the Scheme. While on the face of it this extension to SSP for those shielding for 12 weeks was logical, it sat uncomfortably with the original version of the Treasury Direction which seemed to require SSP entitlement to come to an end before furlough could begin. However, as noted at question 6, above, the amended Treasury Direction appears to allow an employee’s period of incapacity for work, in respect of which they would be entitled to SSP, to be brought to an end by agreement with their employer. This seems to remove the difficulty and make clear that shielding employees can be furloughed by their employer provided the general eligibility requirement that the company’s operations have been severely affected by Covid-19 is met (on which see question 2, above).

For employees who live with someone who is shielding, the Government guidance specifically states that they can be furloughed. Since they are not entitled to SSP, the above inconsistencies between the Government guidance and the original version of the Treasury Direction did not affect your ability to furlough them – although, as is the case for all categories of employee, the general point that the Scheme is intended to be available to companies whose operations have been severely affected by Covid-19 would still apply (see question 2, above).

Although it is unlikely to be relevant in the context of shielding employees and those they live with, most of whom will presumably have been furloughed since quite early on, it is important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. See question 2(a), above and our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, for further details.

6(c). Can an employer furlough an employee who is vulnerable or is otherwise reluctant to come to work for a coronavirus reason, where it otherwise would have work for them to do, but who not does fall within 6(a) and 6(b)? (Last updated 16/06/2020)

This category could include vulnerable employees who may be adhering strictly to social distancing advice and therefore do not feel able to come to work, or employees who are not themselves vulnerable but who live with someone who is and therefore wish to remain away from work to protect that person, or even other employees who are simply unwilling to come into work because they are nervous about being infected.

The Government guidance does not expressly deal with this scenario. In our view, whether or not you can furlough these employees where you would otherwise have work for them to do will depend on the interpretation of references in the Government guidance about the circumstances in which employers can access the Scheme. As noted in question 2, above, this is an area of uncertainty. You will have to make a judgment call based on whether you can say that your operations have been severely affected by Covid-19. If, for example, a business has found that its operations are severely affected, the fact that it still has work for some production operatives to do and it needs to backfill for any of them who cannot come into work should not, of itself, mean that it would not be eligible under the furlough scheme. It is also worth noting that, even if you would otherwise have work for them to do, furloughing employees who are vulnerable or otherwise reluctant to come to work for a coronavirus reason would seem consistent with the requirement in the Treasury Direction that the instruction not to work “is given by reason of circumstances arising as a result of coronavirus or coronavirus disease”.

(Note also that employers may previously have treated vulnerable employees or those who are living with someone who is vulnerable as if they were on sick leave and paying them SSP (and contractual sick pay, if applicable). However, regulations that came into force on 1 April make clear that, strictly speaking, such employees are not legally entitled to SSP. In view of this, employers may have decided to change approach and sought to agree with these employees that they would no longer be treated as on sick leave but would instead be placed on furlough. Similarly, employers that had previously required these employees to take unpaid leave may also have sought to agree with them that they would instead be placed on furlough. However, in this regard, note that the Government guidance states that an employee who is on unpaid leave cannot be furloughed, unless they were placed on unpaid leave after 28 February. It also provides that an employee who went on unpaid leave on or before 28 February cannot be furloughed until the date on which it was agreed they would return from unpaid leave. These points are reflected in the amended Treasury Direction, which also provides that where an employee went on unpaid leave before 1 March, and the employer and employee agreed before 20 March to end that unpaid leave earlier than originally planned, the employee can be furloughed after the agreed varied end-date).

It is important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. See question 2(a), above and our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, for further details.

6(d). What about employees who are on long-term sick leave? (Last updated 16/06/2020)

The Government guidance suggests that you can potentially furlough employees who are on long-term sick leave and it is essentially your decision about whether to do so. However, the original version of the Treasury Direction called this into question as it seemed to indicate that the employee’s entitlement to SSP would first have to come to an end (see question 6, above). This issue seems to have been removed by the amended Treasury Direction which, as noted at question 6 above, appears to allow a period of incapacity for work for which the employee would be entitled to SSP to be ended by agreement between the parties.

However, there remains a degree of uncertainty about whether you can furlough an employee who is currently on long-term sick leave for a non-Covid-19 reason. This is because the Treasury Direction provides that an employee will only be furloughed if (among other things), the instruction that they do not carry out any work “is given by reason of circumstances arising as a result of coronavirus or coronavirus disease”. An employee who is on long-term sick leave for a non-Covid-19 reason is unlikely to meet this requirement. Although the amended Treasury Direction appears to allow sick leave to be brought to an end by agreement in order to access the Scheme, where an employee remains unfit for work due to a non-Covid-19 illness, it seems somewhat artificial to do this and then say that the reason the employee is not working is because of coronavirus. In practice, of course, an employee who remains entitled to full pay company sick pay if they stay on sick leave may be unlikely to agree to end that sick leave in order to be furloughed on a reduced rate of pay. If an employer were to end a period of long-term sick leave in order to furlough an employee, they would also need to consider the implications for the employee’s entitlement to SSP or company sick pay in the future, e.g. if the employee remains unfit for work after the Scheme comes to an end, has their entitlement to sick pay been reset during the furlough period? And what about their position under any trigger system in the employer’s absence management policy?

If, however, the long-term sick leave ends because the employee is fit to return to work, but the employer does not need the employee to work, or there is some other coronavirus-related reason why the employee cannot return, then it should be possible to place that employee on furlough without contravening the Treasury Direction.

It is important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. See question 2(a), above and our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, for further details.

6(e). What if your employee becomes sick while furloughed? (Last updated 26/05/2020)

The Government guidance states that furloughed employees retain their statutory rights, including their right to SSP. This means that furloughed employees who become ill or need to self-isolate because they, or someone in their household, have symptoms of Covid-19 must be paid at least SSP. The Government guidance goes on to say that you can decide whether to move these employees onto SSP or keep them on furlough, at their furloughed rate.

If you keep the sick furloughed employee on the furloughed rate, the Government guidance states that you can still access the Scheme. It may well be more advantageous for the employer to keep the employee on furlough, as furlough pay can be reclaimed from the Government, whilst an employer must pay SSP themselves (although for SMEs with less than 250 employees, up to 14 days’ of Covid-19 related SSP per employee can be reclaimed from HMRC under the SSP Rebate Scheme – see the FAQs on Financial support for your business). Most employees will also be better off staying on furlough, as furlough pay will be higher than SSP. (Note that the amended Treasury Direction’s provisions on sickness and furlough do not appear to prevent this, although they do not address it directly.)

The Government guidance specifies that if you do decide to move a furloughed employee who becomes sick onto SSP, you can no longer claim for the furloughed salary. Nor can you claim for SSP under the Scheme. You can claim back from both the Scheme and the SSP Rebate Scheme for the same employee but not for the same period of time. When an employee is on furlough, you can only reclaim expenditure through the Scheme, and not the SSP Rebate Scheme.

Given the above, employers may be unlikely to move employees off furlough leave and furlough pay onto SSP. However, if they do, the Government guidance does not fully address the consequences of this on the employer’s ability to claim for the employee’s furlough pay under the Scheme. Does it ‘interrupt’ or ‘break’ furlough leave? For example, if an employee falls ill after two weeks on furlough leave, it is not clear whether moving them onto SSP at that point (i.e. before they have been furloughed for three consecutive weeks) would mean that the employer could no longer claim in respect of their furlough pay for the two weeks already spent on furlough? Given the emphasis in the guidance on the three week minimum furlough period, we expect that an employer may no longer be able to claim under the Scheme in those circumstances – and, if so, this is likely to be a significant factor employers will consider when deciding whether to move employees who fall ill during furlough onto SSP.

Where a company operates a contractual sick pay scheme, we would recommend confirming to employees that any company sick pay payable in respect of sickness during furlough will be based on their adjusted rate of furlough pay. (Note, however, that the practical effect of this may be to discourage employees from telling the employer that they are sick, so that they do not use up their company sick pay entitlement.)

6(f). If an employer that had closed its business and furloughed all employees is now reopening, can it keep on furlough any employees who cannot work from home and are unable to return to the workplace? (Last updated 13/05/2020)

The Government guidance on the Scheme does not address this question. However, we assume that an employer whose business had closed due to the Covid-19 pandemic would still be able to satisfy the general eligibility requirement that its business is “severely affected” by coronavirus, even after it reopens. The fact that certain employees are unable to return (e.g. because they are shielding, or otherwise vulnerable) would presumably support this.

As to whether employees in particular circumstances can be furloughed (e.g. those who are shielding, otherwise vulnerable, on sick leave, etc.), see questions 6, and 6(a) to (d), above. Also see the FAQs on ‘Issues at work / on returning to work’ for discussion of points an employer will need to consider when reopening its business.

7. How will furlough leave affect those on maternity leave or due to go on maternity leave? (Last updated 16/06/2020)

The Government guidance states that the normal rules for maternity and other forms of parental leave and pay continue to apply.

Since maternity leave is triggered automatically on the birth of a baby, if not commenced earlier, an employee who gives birth while on furlough would switch to maternity leave and the normal rules around eligibility for Statutory Maternity Pay (SMP) or Maternity Allowance (MA) would apply. If an employee’s earnings have reduced because she has been on furlough leave, this may affect her SMP or MA. However, regulations in force from 25 April 2020 provide that, where an employee starts her maternity leave on or after 25 April 2020, her normal weekly earnings for the purpose of determining her entitlement to, or the amount of, SMP or MA are to be calculated as if she had not been furloughed. Employees on maternity leave must take at least 2 weeks off work (4 weeks if they work in a factory or workshop).

The Government guidance updated on 1 May notes that if an employee is receiving MA through Jobcentre Plus while she is on maternity leave, she should not get furlough pay from you at the same time. Accordingly, if the employee agrees to be put on furlough, you should tell her to contact Jobcentre Plus to stop her MA payments. If the employee agrees to be put on furlough and end her maternity leave early, the Government guidance specifies that she will need to give you 8 weeks’ notice and will only be eligible for furlough pay after the 8 weeks have passed.

Employees who are on maternity leave already, and in receipt of SMP, or no pay in the final 13 weeks of leave, could potentially be better off if they were placed on furlough leave instead and receiving 80% pay. In order to do this, they would have to give notice to end their maternity leave. Although the position under the legislation is that 8 weeks’ notice of return is required, this can usually be reduced by agreement. The employer could then agree with the employee that she would be furloughed, but it would be sensible to make sure she understands that once she has ended her maternity leave she can’t restart it at the end of furlough leave. However, as noted above, the 1 May update to the Government guidance concerning the interaction between furlough pay and MA states that if an employee “agrees to be put on furlough and end their maternity leave early, they will need to give you at least 8 weeks’ notice and they will not be eligible for furlough pay until the end of the 8 weeks”. This strict adherence to the 8 week notice requirement may be necessary in MA cases to allow Jobcentre Plus enough time to stop the employee’s MA payments. It appears under the heading “If your employee gets Maternity Allowance”, so we think it is only intended to apply in MA cases. However, it is possible that this is an oversight and the guidance may be amended further to apply this restriction in other cases as well. If so, this would prevent an employer and employee from agreeing for the employee to return from maternity leave with less than 8 weeks’ notice in order to switch to furlough.

From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees (i.e. those who have been furloughed for at least a 3 week period before the end of June). However, this cut-off date does not apply to employees whom you wish to furlough for the first time on curtailment of their maternity leave, provided you have previously furloughed employees. See question 2(a), above and our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, for further details.

(With regard to employees in the final 13 weeks of their maternity leave, note that the Government guidance states that an employee who is on unpaid leave cannot be furloughed, unless they were placed on unpaid leave after 28 February. It also provides that an employee who went on unpaid leave on or before 28 February cannot be furloughed until the date on which it was agreed they would return from unpaid leave. These points are reflected in the amended Treasury Direction, which also provides that where an employee’s period of unpaid leave began before 1 March and was varied by agreement before 20 March 2020, the employee can be furloughed after their varied agreed date of return from unpaid leave. However, it remains unclear whether these restrictions apply to all types of unpaid leave, including the unpaid part of maternity leave, or only to unpaid lay-off and sabbaticals).

Note that where employees are receiving SMP, employers are already able to claim most of the cost of this back from HMRC, so there is no need for such costs to be covered under the Scheme and the amended Treasury Direction makes clear that employers cannot claim for SMP under the Scheme.

For employees who receive enhanced contractual maternity pay, the position is slightly different. The Government guidance states that you can claim through the Scheme for enhanced (earnings related) contractual pay for women on maternity leave. This seems to allow employees to be on both maternity leave and furlough leave at the same time, but it is not entirely clear and appears to apply a different rule about what furlough pay these employees would receive when compared to other furloughed employees (as it is not based on their pay in the last pay period before 19 March/average previous earnings, but on their contractual maternity pay entitlement). As noted above, the amended Treasury Direction specifies that employers cannot claim under the Scheme for the cost of SMP. Since contractual maternity pay will include an employee’s SMP, employers claiming under the Scheme for the cost of such contractual maternity pay will need to adjust the amount that they are claiming to exclude the SMP element. When considering whether to furlough employees who are in receipt of contractual maternity pay, it is also important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. However, this cut-off date does not apply to employees whom you wish to furlough for the first time on curtailment of their maternity leave, provided you have previously furloughed employees. See question 2(a), above, for further details.

(The guidance provides that the same principles apply where an employee qualifies for contractual adoption, paternity, or shared parental pay.)

Furlough pay for employees who are furloughed on return from family leave is discussed at question 13(b), below.

8. Can an employee ask to be furloughed? (Last updated 16/06/2020)

An employee can ask to be put on furlough leave, but there is no right to furlough, so it is up to the employer whether or not to accede to such a request.

When considering any request to be furloughed, it is important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. See question 2(a), above and our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, for further details.

As well as taking account of the eligibility criteria under the Scheme, employers considering whether or not to place a particular employee on furlough should be aware that equality and discrimination laws continue to apply to such decisions – see further question 9 below.

9. How do you choose whom to furlough if you still have work for some employees to do? (Last updated 16/06/2020)

The Covid-19 crisis means that many employers do not have enough work for all of their employees, but there is still some essential work to be done in certain functions or departments. The Government guidance helpfully notes that employers do not have to put all of their employees on furlough. However, it also makes clear that when employers are making decisions in relation to whom to offer furlough to, equality and discrimination laws will apply in the usual way.

As a first step, employers need to think carefully about what roles they still require employees to perform and the numbers they need in each role. For example, an employer seeking to reduce its shop-floor workforce by 30% will still require a certain number of supervisors to work, in addition to the production operatives.

Having identified the numbers it needs to place on furlough in particular roles, our view is that an employer can probably ask employees to volunteer for this. Doing so may help to reduce any sense of unfairness, as some employees may prefer to continue to work and receive full pay, while others (in particular those who fall into a vulnerable category, or who have childcare needs) may prefer to cease work and remain at home on reduced pay. Assuming that the employer is not proposing to top up employees’ pay above the amount that it can recover from the Government under the Scheme, whether employees would prefer to be furloughed or to continue to work may also be influenced by how much they are normally paid. The Scheme currently covers up to 80% of employees’ gross pay, capped at £2,500 per month (plus the employers National Insurance and minimum auto-enrolment pension contributions on that subsidised furlough pay – see question 13 below). If £2,500 represents 80% of an employee’s gross monthly pay, their full gross monthly pay would be £3,125 per month, or £37,500 per year. Employees whose normal pay is higher than this will suffer more than a 20% pay cut and therefore might be less keen to be furloughed than those for whom the pay cut is limited to 20%. That said, many employees on lower pay may be unable to afford even a 20% pay cut. Accordingly, while we think that most employees would agree to furlough if the alternative is redundancy, they may be less likely to actively volunteer for it if they have the option of continuing at work on normal pay.

Where an employer receives more volunteers than it needs to furlough, or does not receive enough volunteers, it will need to conduct some sort of selection process. The recommended approach may differ depending on whether there are too many or too few volunteers. If an employer has too many employees volunteering to be furloughed, it will need to decide which volunteers to turn down based on which employees have the necessary skills to perform essential retained roles. If an employer has too few employees volunteering to be furloughed, it will have to look at each of the roles for which it has too many employees still wishing to work and apply appropriate selection criteria. As an alternative in either case, the employer may wish to consider rotating groups of employees on and off furlough – see question 17, below.

The safest approach when deciding whom to furlough if you don’t have the right number of volunteers may be to conduct an objective selection exercise in relation to the roles required in order to ensure you retain the best employees but, in reality, practical considerations as to which employees are still able to work, as well as employee relations issues, will probably take precedence. It is also likely that if an employer is in serious financial difficulty and has a really pressing need to furlough employees as soon as possible in order to be able to continue trading, a more limited or cursory approach to the decision may be acceptable. Please email our HR and legal experts or call our National Adviceline on 0333 202 2221 if you need our support.

While employers must take care not to discriminate when selecting which employees to furlough, it is worth noting that certain otherwise discriminatory selection decisions might potentially be justifiable in the circumstances of the Covid-19 crisis. For example, selecting employees aged over 70 could amount to age discrimination. However, it may be possible to justify this as a proportionate means of achieving a legitimate aim – namely, protecting the health and safety of vulnerable employees as identified by the applicable Government guidance.

Employers will also need to keep the situation under review, as they may find that work volumes increase or reduce unexpectedly and they need to bring people back from furlough, or place more employees on furlough, as things evolve. In this regard, it is important for employers to take account of the forthcoming closure of the Scheme to new entrants. From July onwards access will be restricted to employers who are currently using the Scheme and previously furloughed employees. See question 2(a), above and our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’, for further details.

10. What process should you follow to put an employee on furlough? (Last updated 16/06/2020)

In our view, it is important that employees agree to furlough leave as it involves a change in terms and conditions. There had been concern that employers who had simply confirmed to employees that they were being furloughed (following the advice in the early versions of the Government guidance) would be put outside the scope of the Scheme by the original Treasury Direction, which required employees’ written agreement to be furloughed. In view of this, the Government guidance was then updated, apparently in an attempt to tone down the original Treasury Direction, stating that employers must confirm in writing to their employee that they have been furloughed “in a way that is consistent with employment law” and that while there “needs to be a written record… the employee does not have to provide a written response.” However, unless an employer has a contractual right to lay-off, or is maintaining full pay, confirming furlough in a way that is consistent with employment law would – strictly speaking – require the employer to obtain the employee’s agreement (whether or not in writing) in any event. The amended Treasury Direction provides that the employer and employee must have agreed (whether individually or by means of a collective agreement between the employer and a trade union) that the employee will cease all work and that such agreement must:

- specify the main terms and conditions on which the employee will cease work;

- be incorporated (expressly or impliedly) in the employee’s contract;

- be made in writing or confirmed in writing by the employer (such agreement or confirmation may be in electronic form such as an email); and

- be retained by the employer until at least 30 June 2025.

With regard to the requirement to specify the main terms and conditions on which the employee will cease work, we assume that it will be sufficient to cover the extent to which the employee’s normal terms and conditions (e.g. as to pay and benefits) are varied during furlough and any provisions relating to the possibility that the employee may be required to undertake training during furlough, as well as the extent to which they are permitted to work for another employer, or to volunteer. Our template furlough letter covers these points, so we think that employers that have used our template to seek employees’ agreement to be furloughed should meet the requirements of the amended Treasury Direction in this regard. Note that claims under the Scheme made on or after 23 May must be in accordance with the amended Treasury Direction.

In practice, given the unprecedented circumstances of the Covid-19 crisis, it is likely that most employees will agree to furlough, particularly if the alternative is redundancy. Good communication is key in order to encourage agreement. While in-person meetings with all affected staff are unlikely to be possible for most employers in the current circumstances, we would recommend that employers try to arrange some form of meeting (e.g. via Zoom, Skype, or even telephone) at which they can explain to affected employees what they are proposing and the reasons why furlough is necessary, before sending them letters to seek their agreement.

In terms of the mechanics of seeking agreement, where practical, it is best for an employer to write to the employee setting out the proposed move to furlough leave and ask the employee to sign and return a copy of the letter. E-signatures would be appropriate if the company has the necessary software. If e-signatures are not possible, the employer could ask employees to sign and return a hard copy letter. However, if the letter is sent to employees by email, they may not have access to printing and scanning facilities that would enable them to provide this. Accordingly, employers could as an alternative provide for employees to confirm their agreement by email or text message to an appropriate contact at the company (e.g. HR or line manager) using a set form of words, such as “I confirm my agreement to the variation of my terms and conditions of employment to place me on furlough leave as described in the letter from the company dated [DATE]”, or replying to the employer’s email using voting buttons.

Employers that recognise a trade union for collective bargaining with a defined bargaining unit and have a standard incorporation clause in individual contracts of employment should seek to engage with the trade union. In our view, if your collective bargaining arrangements cover changes to pay and hours, then they should also cover furloughing. The fact that the original Treasury Direction referred to agreement between “employer and employee” caused concern for employers that had relied on a collective agreement to furlough employees, as it suggested that an individual agreement would be required in order for employers to make a claim under the Scheme. However, Government guidance for employers was updated on 23 April to confirm that “Collective agreement reached between an employer and a trade union is also acceptable for the purpose of such a claim”. The Government guidance for employees reflects this but also notes that “Once agreed your employer must confirm in writing that you have been furloughed to be eligible to claim” and advises employees to contact their employer if they do not receive such confirmation. Accordingly, if the union agrees, we would suggest that you also communicate/send letters to employees individually, to confirm the change to terms that has been agreed by the union and that it is incorporated into their contracts temporarily. As noted above, the amended Treasury Direction expressly recognises that the agreement to furlough can be a collective agreement between the employer and a trade union.

If an employer with a unionised workforce wants to speed up the process of getting employees’ agreement to furlough, we would suggest that the employer impress upon the union the exceptional and time-critical circumstances. The employer could offer the union a shortened process, for example, one meeting at which the proposal would be discussed and agreement sought. You could also suggest that if the union does not agree then the employer will consider going directly to the employees for their individual agreement. While there is a degree of risk that making direct offers to the employees might contravene section 145B of the Trade Union and Labour Relations (Consolidation) Act, we think this risk is limited given the temporary nature of the proposed contractual changes.

Where a large number of employees is involved and you are not relying on a collective agreement, seeking individual agreement may be time-consuming and administratively burdensome. Pressure of time may mean that employers seeking to place employees on furlough leave need to truncate the normal process they would follow when seeking employees’ agreement to a significant contractual change. Please email our HR and legal experts or call our National Adviceline on 0333 202 2221 if you need our support.

Employers who had placed employees on furlough without agreement, or who had requested employees’ agreement but did not receive it (e.g. if employees did not reply to a furlough letter as requested), might still wish, where practical, to seek individual confirmation from furloughed employees, given that the amended Treasury Direction does still require agreement and there is nothing in it that expressly requires the agreement to pre-date the period of furlough. That said, it has been suggested that a retrospective agreement may not be effective, given the future tense wording of the Treasury Direction, which requires the employer and employee to have agreed that the employee “will cease all work”. In addition, even if employers do write to employees seeking their retrospective agreement to furlough, there is no guarantee that they will respond – positively or at all. In view of this, employers will have to make a judgment call as to whether they try to obtain retrospective individual agreement or seek to rely on whatever original communication they used to confirm employees’ furlough leave (possibly relying on an argument that, by now, employees who have not raised any objection can be taken to have impliedly agreed to being furloughed – although this approach is untested) and wait and see whether HMRC takes issue with that.

(While the Government guidance indicates that if sufficient numbers of staff are involved, it may be necessary to engage collective consultation processes, in our view, it should not be necessary for an employer to initiate collective consultation when first proposing to put employees on furlough leave, unless the employer anticipates that 20 or more employees are likely to refuse – and the consequence for those employees who refuse would be that they are dismissed. Furlough is likely to be an attractive option for most employees, so employers would be unlikely to anticipate 20+ refusals at the outset).

(Also note that if furloughing a company director, the company board must formally adopt the decision, note it in the company records and communicate the decision to the company director concerned.)

For details of the process to follow when placing an employee back on furlough, or agreeing that an employee will work part-time during furlough under the Revised Scheme, see our FAQs on ‘Furlough under the Revised Coronavirus Job Retention Scheme’.

11. What happens to an employee’s terms and conditions of employment during furlough leave? (Last updated 26/05/2020)

In theory, an employer could agree any changes it wishes with the employees it places on furlough. But in practice, the more severely the employer tries to remove or restrict benefits during furlough leave, the more likely it is that employees might refuse to agree to the proposed changes. Employees may be more likely to agree to otherwise unpalatable changes where the employer is in difficult financial circumstances and can clearly explain to employees the need for particular changes in order to help the company continue as a viable business. In all cases, however, it is important for the employer to communicate with its employees so that they understand the changes the employer is seeking to make and why it needs to make them.

Employers cannot place employees on furlough without their agreement, so will need to weigh up the importance of additional contractual changes against the likelihood of employees refusing to agree – and the potential complications that will cause (see question 12, below). As noted at question 10, above, the amended Treasury Direction requires the agreement to furlough to specify the main terms and conditions of the furlough leave, so any changes the employer does wish to make should be specified when placing the employee on furlough.